Behind closed doors in a small office, off an nondescript corridor, in a rather large building on Rue Wiertz in Brussels, Belgium a hushed conversation took place last month. Shortly afterwards a piece of European Parliamentlegislation was quietly shelved. It carried the rather dull title of “Directive 2009/125/EC” and it was one of the most dangerous documents in Europe!

What was so dangerous about Directive 2009/125/EC, or to give it its full title, “Establishing a framework for the setting of ecodesign requirements for energy-related products”? Directive 2009/125/EC was planning to ban high-powered kettles across Europe to reduce carbon emissions. At the last minute the rulers in Europe realised that banning high powered kettles from the British, the world’s greatest tea drinkers, would cause a literal storm in a tea cup. Not helpful at a time when the UK people are about to vote on whether to leave the European Union!

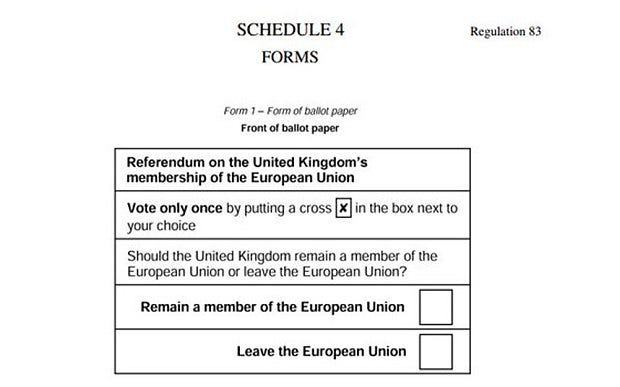

The Referendum

That’s right. On 23 June 2016 the 50m people of voting age in the United Kingdom (including myself!) will all collectively be asked one simple question…

The stakes couldn’t be higher. The outcome will not only decide Britain’s future but Europe’s too and, as the world’s 5th largest economy, the fallout will be felt around the globe.

It’s a historic occasion too, being the first time we’ve been given a choice on Europe since the 1975 EEC referendum. Back then it was a vote on a European Economic Community, an economic and trading integration of the member states. It has since evolved into a political, and for some EU states monetary, union. It’s this political union and the ever closer integration part that has got some people upset, so much so that UK Prime Minister David Cameron deemed it necessary to promise the UK people a referendum on the matter to help secure the last election.

It’s going to be an interesting few months with campaigns hard fought on both sides over the usual issues of immigration, economy, trade, sovereignty & welfare. There will be facts, made-up facts, fear mongering, finger-pointing, vested interests, sleaze and all the the other window-dressing you’d expect from such a high stakes process. At the end of the day the UK is a democracy and it’s up every UK citizen to make their own minds up on 23rd June.

From my perspective and given my role as a top global FinTech influencer, I’ve been asked many times recently about the impact on the blossoming UK FinTech (Financial Technology) industry should the UK vote to leave the EU. So let’s look specifically at what a brexit would mean for #FinTech…

What would a Brexit mean for UK FinTech?

If there’s one thing we in the UK are rather good at (other than drinking tea!) it is Banking. London has always been a global financial centre for historical, cultural and geographical reasons and according to an independent reportpublished last month the UK is now the world’s leading #FinTech centre too! What would happen to UK #FinTech should we leave the EU?

Let’s start by looking at a more relevant EU Directive 2014/49/EU which came into place on 1st January this year. Up until this point the UK’s Financial Services Compensation Scheme (FSCS) protected individuals’ bank deposits up £85,000. On 1st January 2016 the FSCS limit was slashed from £85k to £75k to adhere to directive 2014/49/EU European Union Deposit Guarantee Schemes Directive (EDGSD) which harmonised the deposit protection to limit to €100,000 (or the equivalent) across Europe. Long story short — UK depositors are less protected because of an EU rule overriding a UK rule.

Let’s look at another EU Directive 2015/2366/EU, the amended Payment Services Directive or “PSD2” as it’s fondly referred to in banking circles. This was formally adopted last November and gives EU banks until 13th January 2018 to basically get onboard with APIs, with the view to making banking more transparent/competitive/open. For incumbent banks, PSD2 is a pain in the bum but for the wider FinTech industry and consumers it is generally viewed as a positive force. So here we have an example of a EU doing something the UK Financial Services regulators really should have put in place themselves.

PSD2, EDGSD, GDPR, etc etc etc — the list of directives goes on. Some are good for the UK, some are bad. Some overrule existing UK laws, some create new ones. Some are generally viewed as sensible and some seem like downright interference. On rare occasions EU member states manage to negotiate opt-outs on directives (the UK has 4 opt-outs in place right now) but they are hard fought. It all comes down to sovereignty, the right to govern oneself. Whether the directives are good or bad for the UK the fact of the matter is that it is no longer the UK parliament that gets to make the rules. If the UK is to continue to lead the world in #FinTech the loss of sovereignty is quite frankly a liability.

It’s not just the endless stream of directives lobbed across the English Channel that is concerning, it’s the opacity of the whole organisation. According to a study commissioned by the European Parliament and released last month,the EU has a corruption problem that could cost it up to €990 billion a year. The EU’s accounts consistently don’t add up with more than €133.6 billion of European Union budget payments last year “affected by material error”. The European Central Bank (ECB) said last October that Greece’s banks need more than €14bn in fresh capital, the latest in a long string of bailouts seen by many as an exercise in saving-face and keeping the European single currency dream alive rather than helping Greeks. Throw into the mix the European Financial Transaction Tax (FTT)- a clear and present danger to London’s dominance as a global trading hub. The whole situation is best summed up by this verse from Coolio’s 1995 Gangsta’s Paradise:

Power and the money, money and the power

Minute after minute, hour after hour

Everybody’s running, but half of them ain’t looking

What’s going on in the kitchen, but I don’t know what’s cooking

Brussels is the kitchen and I don’t know exactly what is being cooked up but from what I can see it stinks!

On the most part I think we in the UK are rather good at critical thinking. Perhaps its a natural cynicism but when characters like Obama come over and tell us we should stay in the EU something doesn’t feel right. There have been a string of influential business and political leaders who have come out recently and recommended staying in the EU but these people all have vested interests in maintaining the status quo. I’m also deeply worried by rumours of gagging of experts. For example John Longworth, Chief of British Chambers of Commerce left his position last month, citing need to ‘express my own views freely’ on the EU referendum debate. Whether John is for/against a Brexit I don’t know but either way at times like this we need experts such as John to be free to tell us what they think.

What would a Brexit look like?

The simple answer is that nobody knows for sure. There are plenty of phrases in the English language to sum up fear of change.

"Better the devil you know."

"Out of the frying pan and into the Fire."

"The Grass isn’t always greener on the other side."

What they all mean is that it’s easier to stick with something you know, even if not ideal, than to try changing the situation and risk making it worse. It’s exactly this fear of the unknown which sums up the arguments of the “Stay’ campaigners. It’s easier to calculate the costs/benefits of being in the EU than to quantify the risks of leaving.

I fear we have got ourselves into a boiling frog situation. The 1975 EEC referendum was a vote for a trade union and since then, through regulation after regulation, treaty after treaty, directive after directive, the EU has expanded its remit to become a beast. The argument could be flipped around — if the EU is a burning platform or a sinking ship at what point should you jump off?

We have some other phrases in the English language:

Nothing ventured nothing gained

Who dares, wins

You have to speculate to accumulate

I believe it is time we started treating a Brexit as an opportunity, not just for UK FinTech but for the UK as a whole. It’s like a choice myself and a good few people in the London FinTech scene have made — do you continue working for a large incumbent organisation or quit and join a startup. Well I believe it’s time the UK started acting more like a startup and less like an employee of Europe.

An Exit Strategy

If we wake up on 24th June on an EU exit trajectory here is what I propose happens.

1. A Directive Buffet

An immediate audit is conducted of all the EU rules/directives, sorting them into 3 piles — Keep, Drop, Change. E.g for PSD2 our FCA may well decide to continue the pressure on the big UK banks to open up APIs.

2. Put a bouncer on the Door

Immigration has been a huge part of the wider Brexit debate but I’m not one for bricking up the channel tunnel and pulling up the draw-bridge. Immigration is good. As far as FinTech/Banking is concerned I suggest we immediately identify key talents/skills we need in the UK and put measures in place to fast-track entry.

3. Become the new “offshore”

The UK has a stable political, legal and financial system which makes it a good place to do business. With the new-found freedom the UK should take this to the extreme and begin courting the world’s large enterprises and startups to come set up HQ in the UK. It’s good timing too given scandals like the Panama Papers! We can start by reducing business rates.

The UK has a stable political, legal and financial system which makes it a good place to do business. With the new-found freedom the UK should take this to the extreme and begin courting the world’s large enterprises and startups to come set up HQ in the UK. It’s good timing too given scandals like the Panama Papers! We can start by reducing business rates.

4. Forge new alliances

The EU is not the only club the UK is a member of right now and and the EU is not the only place we trade with. Leaving the EU gives the UK more political freedom to strengthen alliances outside of the EU, e.g. with Israel and theirburgeoning FinTech hub in Tel Aviv and rekindle historical relationships, e.g. with India. At the same time we should be helping other dissatisfied EU members, e.g. Denmark, should they wish to make similar exit plays and providing a ‘life boat’ to those citizens that ‘want out’

5. Play to win

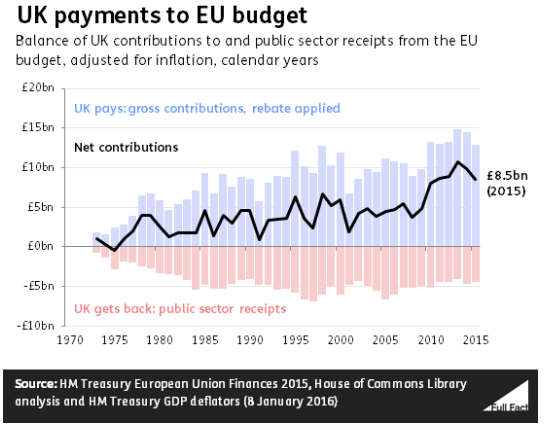

Time for a mindset change. Instead of squabbling for the scraps from the EU table the UK has the opportunity to reinvent itself like a startup`. We’re the 5th largest economy in the world in-spite of being in the EU, not because of it. Given the freedom from EU red tape the UK should put in place measures to target 4th place by the end of the decade. We can start by taking our£23,000,000/day EU membership fee and investing it in UK enterprise!

Summary

The world is a very different place to when the EEC was set up in 1975. The EU was formed to solve the problems of the last century, but it has overstepped its mark and lost its way. The 21st century challenges are more digital. Things like individual freedom/privacy, security/influence, cyber crime/warfare, resource scarcity/allocation, knowledge economies, sharing economies. These issues are being decided online, by individuals and big corporations, not in the EU Parliament buildings. We are lucky in the UK to have an education system that encourages creative thinking over rote learning. It has spawned some of the great thinkers and doers throughout history and fuelled the British Empire. Those days are gone but who’s to say we can’t turn the UK into a Digital Empire — starting with #FinTech/Banking and expanding to other industries.

The EU is a burning platform and it’s time the UK got off — for the sake of UK FinTech and the UK in general I believe now is the right time to leave the EU.

Chris Gledhill

The world is a very different place to when the EEC was set up in 1975. The EU was formed to solve the problems of the last century, but it has overstepped its mark and lost its way. The 21st century challenges are more digital. Things like individual freedom/privacy, security/influence, cyber crime/warfare, resource scarcity/allocation, knowledge economies, sharing economies. These issues are being decided online, by individuals and big corporations, not in the EU Parliament buildings. We are lucky in the UK to have an education system that encourages creative thinking over rote learning. It has spawned some of the great thinkers and doers throughout history and fuelled the British Empire. Those days are gone but who’s to say we can’t turn the UK into a Digital Empire — starting with #FinTech/Banking and expanding to other industries.

The EU is a burning platform and it’s time the UK got off — for the sake of UK FinTech and the UK in general I believe now is the right time to leave the EU.

Chris Gledhill

CEO, Founder

No comments:

Post a Comment